Have you ever found yourself tangled in the maze of real estate jargon while buying a home? You’re not alone.

Many homebuyers are puzzled by terms like “earnest money” and “down payment. ” Are they the same thing? Do they serve the same purpose? Understanding the difference can make a huge impact on your home-buying journey. Imagine stepping into your dream home, confident in every financial decision you’ve made along the way.

This knowledge isn’t just helpful; it’s empowering. Let’s clear up the confusion and give you the clarity you need to make smart, informed choices. Stick around, and you’ll soon be navigating the world of real estate like a pro.

Earnest Money Basics

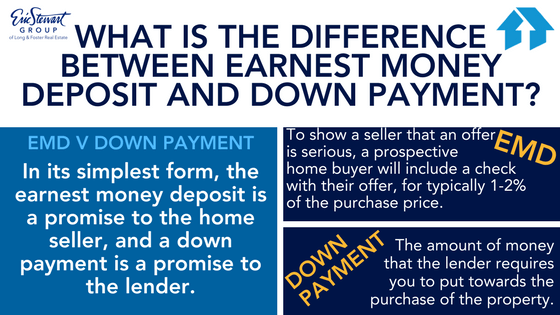

Earnest money shows a buyer’s serious intent. It protects the seller. If the buyer backs out, the seller keeps the money. The money is held by a third party. This is usually a real estate agent or lawyer. The funds are kept in a safe account. The money is part of the offer. It shows the buyer won’t change their mind easily. It assures the seller the buyer is committed. It’s not the same as a down payment.

Earnest money is usually 1% to 3% of the home’s price. For a $200,000 home, it could be $2,000 to $6,000. This amount can vary by location. Higher amounts show more seriousness. Sometimes, sellers ask for more. Bigger amounts can also make offers stronger. This helps in competitive markets. Buyers should budget for this cost.

Down Payment Essentials

Down payments are needed for buying a home. They show that you are serious. This money reduces the loan amount. Lenders feel safer with a down payment. It lowers the chance of losing money. Buyers with a down payment get better loan terms. They might pay less interest. A bigger down payment means smaller monthly payments. This is why down payments are important.

The typical down payment is a small part of the home’s price. Often, it is around 20%. Some buyers pay less. They might pay only 3% to 5%. It depends on the loan type. With a smaller down payment, buyers might need insurance. This is called mortgage insurance. It protects the lender. Paying more upfront can save money later. Bigger down payments mean less interest over time.

Key Differences

Earnest money is given at the start. It’s like a promise. Down payment is given at closing. It helps you buy the home.

Earnest money shows you’re serious. It holds your place. Down payment reduces your loan. It shows how much you can pay now.

Earnest money doesn’t change your loan size. It’s returned or goes to the cost. Down payment lowers your loan. It affects your monthly payments.

Refundability And Risks

Earnest money can be refunded under certain conditions. If a buyer backs out due to a failed inspection, they may get their money back. Sellers may refund earnest money if financing falls through. Buyers should understand all contract terms. These terms outline when a refund is possible. Not understanding can lead to a loss of money.

There are risks with earnest money. Buyers might lose it if they break the contract. Missing deadlines can also be risky. Sellers may keep the money if buyers change their mind. Buyers should know all potential risks. Reading the contract carefully is vital. Understanding risks helps avoid losing money.

Impact On Buyers And Sellers

Earnest money serves as a financial commitment showing a buyer’s interest, while a down payment secures loan approval. Buyers need to understand the distinction to manage funds wisely. Sellers benefit from earnest money, as it indicates serious buyers, reducing potential sales fall-throughs.

Buyer Considerations

Earnest money is a small amount paid first. It shows the buyer is serious. This money goes to the seller if the buyer backs out. It’s not the down payment. The down payment is much bigger. It’s given at the end to own the home. Buyers must plan their budget well. They need enough for both earnest and down payments. Always know the terms of the deal. This way, they avoid losing their earnest money.

Seller Considerations

Sellers see earnest money as a promise. It means the buyer wants the house. If the buyer changes their mind, sellers keep this money. It helps them if they lose other buyers. But, sellers must be fair. They should follow the rules in the agreement. This builds trust and helps the deal go smoothly.

Practical Tips

Earnest money and a down payment are not the same. Earnest money shows a buyer’s commitment. A down payment is part of the purchase price. Both are important in real estate transactions. Understanding the difference can help in planning your home purchase effectively.

Negotiating Earnest Money

Earnest money shows you are serious about buying. It helps secure the deal. Sellers feel more confident with earnest money. Always discuss the amount with your agent. Try to offer a reasonable amount. This shows respect for both sides. Ask questions about how the money is used. Make sure you understand the terms. You should know if you get it back if the deal fails. Always read the contract carefully. Check for any hidden rules. It’s smart to ask for help if confused.

Planning Your Down Payment

Down payment is part of the home cost. It is not the same as earnest money. Save money early for a good down payment. This can lower your loan amount. Talk to lenders about payment options. They can give good advice. Different loans need different down payments. Understand what each loan needs. Compare each option to pick the best one. Make a budget for your future. It helps in saving more money. You can reach your goal faster.

Frequently Asked Questions

What Is Earnest Money In Real Estate?

Earnest money is a deposit made by a buyer to show serious intent. It’s typically 1-3% of the purchase price. This deposit is held in an escrow account until closing. It demonstrates the buyer’s commitment to the purchase.

How Does Earnest Money Differ From A Down Payment?

Earnest money is a good faith deposit, while a down payment is part of the purchase price. The earnest money is paid upfront to secure the offer. The down payment is paid at closing and is usually a larger amount.

Can You Lose Your Earnest Money Deposit?

Yes, you can lose your earnest money if you back out of the deal. If contingencies are not met or deadlines are missed, the seller may keep the deposit. However, if the sale falls through due to unmet conditions, you may get it back.

Is Earnest Money Refundable?

Earnest money is often refundable if certain conditions are not met. If the buyer withdraws within the contingency period, it is usually refundable. However, if the buyer defaults on the contract, the seller might keep it.

Conclusion

Understanding earnest money and down payments is crucial in real estate. They serve different purposes. Earnest money shows the buyer’s commitment. A down payment is part of the purchase price. Knowing the difference helps buyers plan finances better. Misunderstanding these can cause confusion.

Ensure you budget correctly for both. This knowledge aids in smoother transactions. Always consult a real estate professional for advice. This ensures informed decisions when buying a home. Make your home-buying journey less stressful.