Are you considering buying a motorcycle but unsure about how much you need for a down payment? You’re not alone.

Many potential buyers like you are curious about what the average down payment on a motorcycle is and how it can impact their purchase decision. Understanding this key financial component can not only help you plan your budget better but also make the dream of owning a motorcycle more attainable.

We’ll unravel the mystery surrounding motorcycle down payments, ensuring you’re well-informed and confident as you rev up your buying journey. Stay with us, and discover how a little knowledge can go a long way in securing the ride of your dreams.

Understanding Down Payments

Buying a motorcycle often means making a down payment. This is the first payment before monthly installments. Dealers usually ask for 10% to 20% of the bike’s price. A larger down payment can mean lower monthly costs. It shows commitment to buying. Some people choose to pay more upfront. This reduces the total interest paid. Saving money for the down payment is important. It can help in getting a better deal. Always check your budget before deciding. Knowing your budget helps in choosing the right motorcycle.

Factors Influencing Down Payments

Credit Score is very important. A high score means lower payments. A low score can mean higher payments. Lenders trust good credit scores more.

The type of motorcycle can change the payment. Sports bikes may need bigger payments. Simple bikes might need less. The cost of the motorcycle affects the payment size.

Loan terms and conditions also matter. Shorter loans need bigger payments. Longer loans can mean smaller payments. Always check the loan details.

Typical Down Payment Percentages

Buying a new motorcycle often needs a higher down payment. This is usually around 10% to 20% of the bike’s price. New bikes cost more, so the payments are bigger. Used motorcycles might need less money upfront. 5% to 15% is common for used ones. Prices for used bikes are lower, so payments are smaller. It helps buyers save more money.

Dealers might have different suggestions. They know about the best deals. Some dealers might say 20% down is good. Others may accept only 10%. It depends on the bike and the dealer. Asking dealers for their advice can help. Always check multiple dealers for the best offer.

Financing Options

Bank loans can help buy a motorcycle. They offer fixed interest rates. Monthly payments are predictable. It’s easy to plan your budget. Some banks need a good credit score. Others need proof of income. Check different banks for the best deal.

Credit unions are another choice. They often have better rates. Members get special benefits. Joining a credit union is easy. They focus on helping local communities. Your credit score matters here too. Compare offers from various credit unions.

Manufacturer financing helps if you want a new bike. Companies offer special deals. They give low interest rates. Some offer zero down payment options. This can save money upfront. Always read the terms carefully. Understand the total cost before deciding.

Strategies To Lower Down Payment

A good credit score helps lower your down payment. Paying bills on time is crucial. Keeping credit card balances low is also important. Request a free credit report each year. Look for errors and fix them quickly. This raises your score over time. A higher score means a smaller down payment.

Talk to the seller about payment options. Ask for a lower down payment. Offer to pay more each month. This can help lower the upfront cost. Always read the contract carefully. Understand all terms before signing. Sellers want to make a deal. Use this to your advantage.

Some dealers offer special incentives to reduce costs. These can include lower down payments or discounts. Always ask about current offers. Manufacturers might have seasonal deals. These can help save money. Look for trade-in programs too. They can reduce the amount you need to pay upfront.

Considerations For First-time Buyers

Saving for a motorcycle takes time. Set a clear budget. Know how much you can save each month. Open a savings account. Put money in it regularly. Cut unnecessary expenses. Use this money for your bike. Plan for emergencies. Keep a small fund aside. This helps if costs go up. Stay focused. Remember your goal.

Buying a motorcycle involves more than the down payment. Insurance costs add up. Monthly payments can change. Maintenance fees come often. Fuel expenses are regular. Gear and accessories are needed. Consider all these costs. Compare prices before buying. Make sure you understand each cost. Ask questions if unsure. Be ready for surprises.

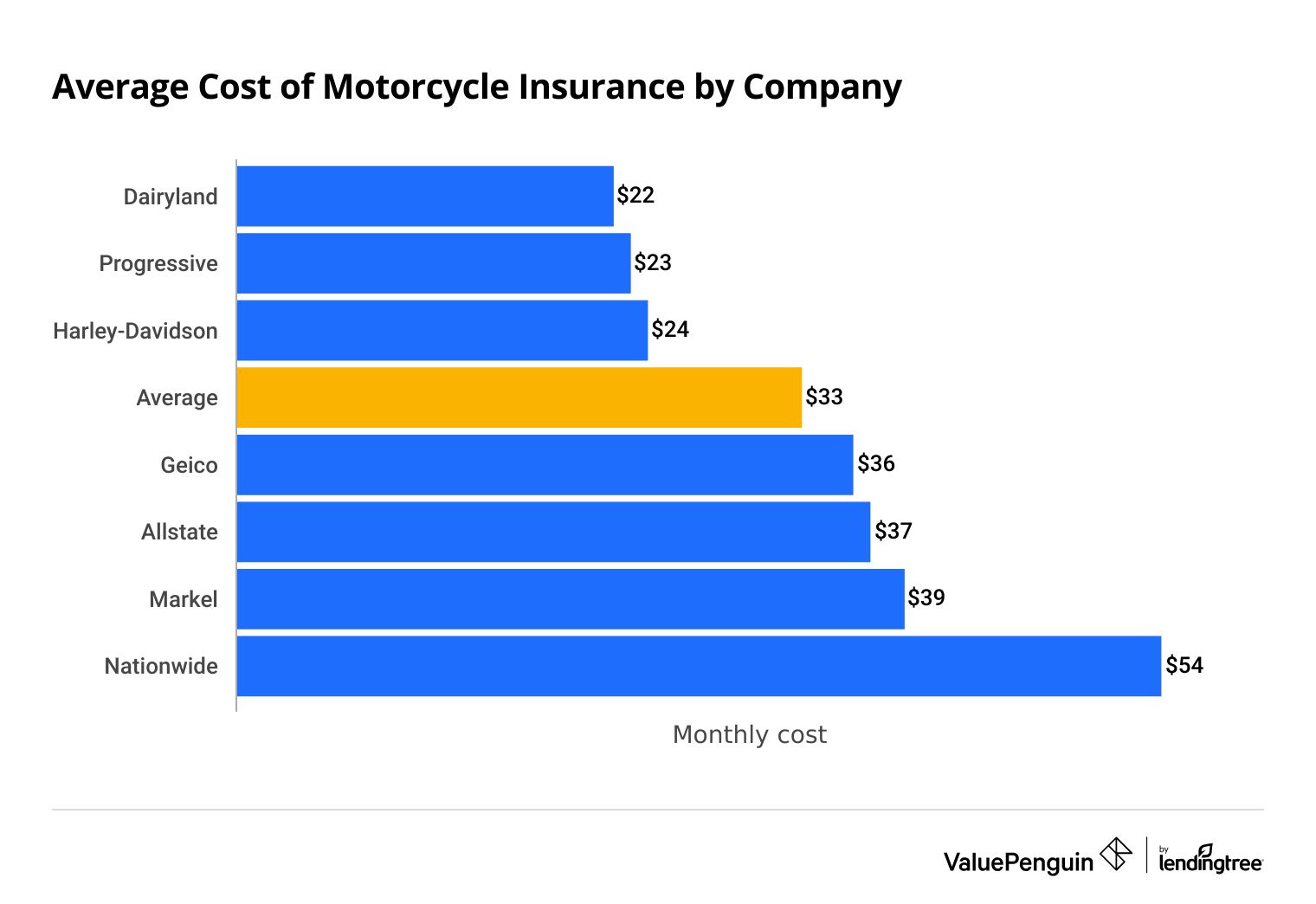

The Role Of Insurance

Motorcycle buyers often wonder about the average down payment. Typically, it ranges from 10% to 20% of the purchase price. This percentage helps buyers secure financing, making monthly payments more manageable.

Insurance Requirements

Most motorcycle buyers need insurance. It’s important. States have laws about insurance. You must have it. Insurance protects you. It also protects others. Without insurance, you can get fines. Your motorcycle can be taken away. Insurance keeps you safe. It also helps in accidents.

Cost Implications

Insurance costs money. Every month, you pay for it. The cost depends on many things. Your motorcycle type matters. Your driving record matters too. Some insurance is cheap. Other insurance is expensive. It’s important to compare prices. Always look for the best deal. Insurance is part of the motorcycle cost. Budget for it. Don’t forget.

Frequently Asked Questions

What Is A Typical Down Payment For A Motorcycle?

The typical down payment for a motorcycle is around 10% to 20% of the purchase price. This can vary depending on the lender and your credit score. Making a higher down payment can reduce your monthly payments and overall interest costs.

Can I Buy A Motorcycle With No Down Payment?

Yes, some lenders offer no down payment options for motorcycle purchases. However, this may result in higher interest rates and monthly payments. It’s essential to evaluate your financial situation and consider making a down payment to save on total loan costs.

How Does Credit Score Affect Motorcycle Down Payment?

Your credit score significantly influences your motorcycle down payment. A higher credit score may allow you to make a lower down payment. Lenders view higher scores as less risky, potentially offering better loan terms and interest rates.

Are There Financing Options For Bad Credit?

Yes, financing options exist for those with bad credit, but terms may be less favorable. You might face higher interest rates and larger down payment requirements. Improving your credit score can help secure better financing options for your motorcycle purchase.

Conclusion

Understanding the average down payment on a motorcycle helps you plan better. Most buyers put down 10% to 20% of the bike’s price. This varies based on your credit and the dealership’s policy. Save up and consider all financing options.

A larger down payment means lower monthly payments. This also reduces interest over time. So, aim for a comfortable amount you can afford. Research thoroughly and make an informed decision. Owning a motorcycle is a big step. Enjoy the ride responsibly!