Puis-je obtenir un prêt sur titre tout en effectuant mes paiements ? Découvrez comment.

Are you juggling monthly car payments and wondering if you can still get a title loan? You’re not alone.

Many people find themselves in a similar situation, searching for a financial lifeline without disrupting their existing commitments. Understanding the ins and outs of title loans while still making payments can be the key to unlocking the financial flexibility you need.

We’ll dive into what you need to know before making this decision. You’ll discover how you can potentially access funds without losing control over your vehicle. Keep reading to find out how you can navigate this financial path safely and efficiently.

Understanding Title Loans

Thinking about title loans while still making payments? It’s possible, but check lender terms first. They usually consider the remaining loan balance and your repayment history. Always understand the risks and obligations before proceeding.

What Are Title Loans?

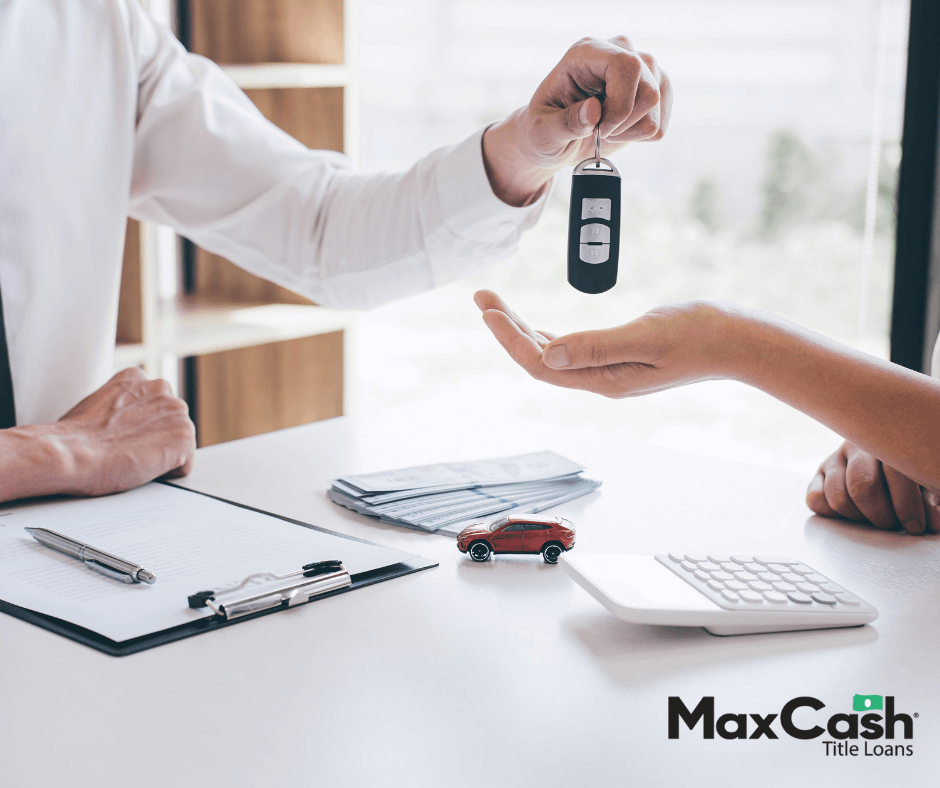

Title loans are loans where you use your car title as a promise to pay. They are short-term loans. People get them when they need money quickly. You must have a car in your name to get a title loan. The car must have no other loans on it. These loans have high interest rates. This means you pay a lot more than you borrow.

How Title Loans Work

To get a title loan, you show your car title to the lender. The lender checks your car’s value. They give you a loan based on this value. You keep your car while you pay back the loan. But if you do not pay, the lender can take your car. The loan usually lasts for 30 days. You must pay back the loan within this time. If not, you may lose your car.

Eligibility For Title Loans

To get a title loan, own a vehicle. The car must be in your name. You need a clear title. This means no one else claims the car. Show proof of revenu. This helps the lender trust you. Sometimes, a photo ID is required. This shows who you are. These are the basic needs for a title loan.

Existing vehicle loans can affect your chances. Some lenders allow it. Others want a clear title. This means no loans on the car. With a loan, the car’s value might be less. This affects the loan amount. It’s important to check with the lender. Each one has different rules.

Applying For A Title Loan With Existing Payments

Check your loan details. Know your monthly payments and interest rate. Understand how much you still owe. This helps plan your next steps. Make sure your budget can handle another loan. Your car’s value is important. It affects the loan amount you can get. Consider your car’s age and condition. These factors play a big role. Getting a title loan needs careful planning.

Talk to your lender about your plans. Explain your current loan status. Tell them you need a title loan. Ask if they offer title loans. Ask about their rules and requirements. Some lenders may help you. Others might have strict conditions. Clear communication is key. It helps you know your options. Understanding their terms is crucial. This ensures you make smart choices.

Risks And Considerations

Potential Financial Strain can happen with title loans. You must pay two loans. This means more money going out each month. Paying two loans is hard for many people. It can lead to less money for food and bills. Budgeting becomes tough. Missing payments can happen easily. This adds extra stress. You should think carefully before getting a title loan.

Repossession Risks are serious. If you miss payments, the lender may take your car. Losing your car means losing your main way to travel. This can affect your job. Getting to work becomes harder. Family life may get disrupted too. Always check the terms of the loan. Ask about repossession rules. Understand what happens if you can’t pay. This helps you make a safe choice.

Alternatives To Title Loans

Banks and credit unions offer prêts personnels. They are a good choice for many people. Personal loans have fixed rates. Monthly payments stay the same. This helps with planning your budget. Check your credit score first. A higher score means better rates.

Credit cards can be useful too. Some have 0% intérêt for a limited time. This can help if you pay off the balance quickly. Remember, credit cards have high interest rates after the special period. Be careful with spending. Only buy what you need.

Borrowing from family or friends can be a good option. This often has no interest. But, it’s important to talk first. Agree on how and when to pay back. Keep the promise to avoid problems. Trust is important in families and friendships.

Tips For Managing Multiple Loans

Créer un budget is very important. It helps control your money. Start with listing all your dépenses. Include rent, groceries, and loan payments. Compare it to your revenu. Make sure expenses don’t exceed income. Piste your spending weekly. This shows where you spend too much. Adjust your budget if needed.

Focus on paying loans first. Choose loans with highest interest rates. Paying them early saves money. Always make the paiement minimum for all loans. This avoids late fees. If possible, pay extra on highest interest loan. Reduce spending on non-essentials. Use saved money for extra loan payments.

Final Thoughts On Title Loans

Title loans can be a useful option. They help when you need quick cash. Car titles are used as collateral. Payments can still be made. These loans are short-term. Interest rates are often high. Understand the terms before agreeing. Read the contract carefully. Always know your payment schedule. Missing payments can be risky. Lenders might take your car. Consider all options before deciding. Speak with a financial advisor. They can offer guidance. Research various lenders. Compare their rates and conditions. Choose the best fit for your needs. Always plan your budget wisely. This ensures you can repay on time.

Questions fréquemment posées

Can I Get A Title Loan With Existing Payments?

Yes, you can get a title loan while still making payments on your car. The lender might assess your car’s equity and your ability to repay. It’s crucial to check the lender’s requirements and ensure you can manage both loan payments without financial strain.

What Are The Requirements For A Title Loan?

The requirements for a title loan typically include a clear car title, proof of income, and identification. Lenders may also evaluate your car’s value and your ability to repay. Each lender might have specific criteria, so it’s essential to verify their terms before applying.

How Does A Title Loan Affect My Car Ownership?

A title loan uses your car as collateral, but you retain ownership. If you default on payments, the lender may repossess your vehicle. It’s crucial to understand loan terms and ensure timely payments to avoid losing your car.

Are Title Loans Available For All Vehicles?

Title loans are generally available for most vehicles, but conditions apply. The vehicle must have enough equity and be in good condition. Some lenders may have specific requirements regarding the car’s age, mileage, and value. It’s best to check with individual lenders for their criteria.

Conclusion

Navigating title loans while making payments can be tricky. It’s important to assess your financial situation carefully. Understand the terms before committing to a new loan. Communicate with your current lender about your plans. They might offer helpful advice or options.

Consider the interest rates and repayment terms of the title loan. Ensure it aligns with your budget. Seek professional financial advice if you’re unsure. Making informed decisions can prevent future financial strain. Always prioritize your financial well-being. Stay informed and choose wisely.