¿Cuántos pagos faltan hasta el repo? Guía esencial

When you’re juggling multiple financial responsibilities, it’s easy to feel overwhelmed. Bills, loans, and unexpected expenses can sometimes make it challenging to keep up with your car payments.

You might be wondering, “How many payments can I miss before my vehicle is repossessed? ” This is a crucial question that can impact your financial future and your daily life. We’ll explore the factors that influence repossession timelines, so you can take control of your situation before it spirals out of control.

Understanding these details can empower you to make informed decisions and potentially save your vehicle from being taken away. Stay with us as we break down this complex topic into simple, actionable insights that can make all the difference for you and your family.

Understanding Auto Loan Repossession

Repossession happens when you do not pay your car loan. The bank takes back the car. This is because the bank wants its money back. The car is a guarantee for your loan. If you miss payments, the bank gets worried. They think you might not pay at all. So, they take the car and sell it. They use the money to cover your missed payments. This is called repossession. It is a serious matter. It affects your credit score. People should avoid this situation.

Missing payments is a big trigger. Banks wait for two or three missed payments. After that, they take action. They might call you or send letters. They warn you about losing your car. Ignoring these warnings is risky. Late payments can also trigger repossession. Even paying late a few times is bad. Banks see it as a pattern. They think you might not pay in the future. This makes them act fast. Keeping up with payments is very important.

Financial Impact Of Missed Payments

Missing car payments is serious. It can reducir su puntuación crediticia. Credit scores show how well you pay back money. A lower score means you might pay more for loans. It can also affect getting a new job or house. Banks might think you won’t pay them back. So, it’s important to pay on time.

Missing payments can have long-term effects. Cars might get taken back if payments are missed. This is called repossessed. You might also owe more money to the bank. It can be hard to get another car loan. Paying late fees can add up. Always make sure to pay on time to avoid trouble.

Repo Timeline And Process

Missing a payment can lead to a recuperación. Usually, the lender waits two to three months. Each lender has different rules. Some act after one missed payment. Others wait longer. It’s important to know your lender’s policy. This helps you plan better. Keep track of your payments. Avoid missing them if possible. Contact your lender if you struggle. They might offer help or a new plan.

The process starts when you miss payments. First, the lender sends a notice. This warns you about the missed payment. Next, they might call or send letters. Then, they may hire a repo agent. This agent takes the car back. After repossession, the car may be sold. The money covers the loan. Anything leftover might go back to you. Stay informed about each step. This helps you stay prepared.

State Laws And Regulations

Leyes estatales about repossession differ a lot. Some states allow quick repossession. In other places, laws are strict. Lenders must follow rules. They need to send notices first. Timeframes vary between states. One state might allow action after two missed payments. Another might wait for three or more. Knowing your state’s law is very important. It helps protect your rights.

Consumers have rights during repossession. Lenders can’t use force. They must act fairly. Personal belongings inside a car must be returned. Some states provide extra protections. You might get a chance to pay what’s owed. Or make a new payment plan. Understanding these protections can help. It keeps you informed and ready.

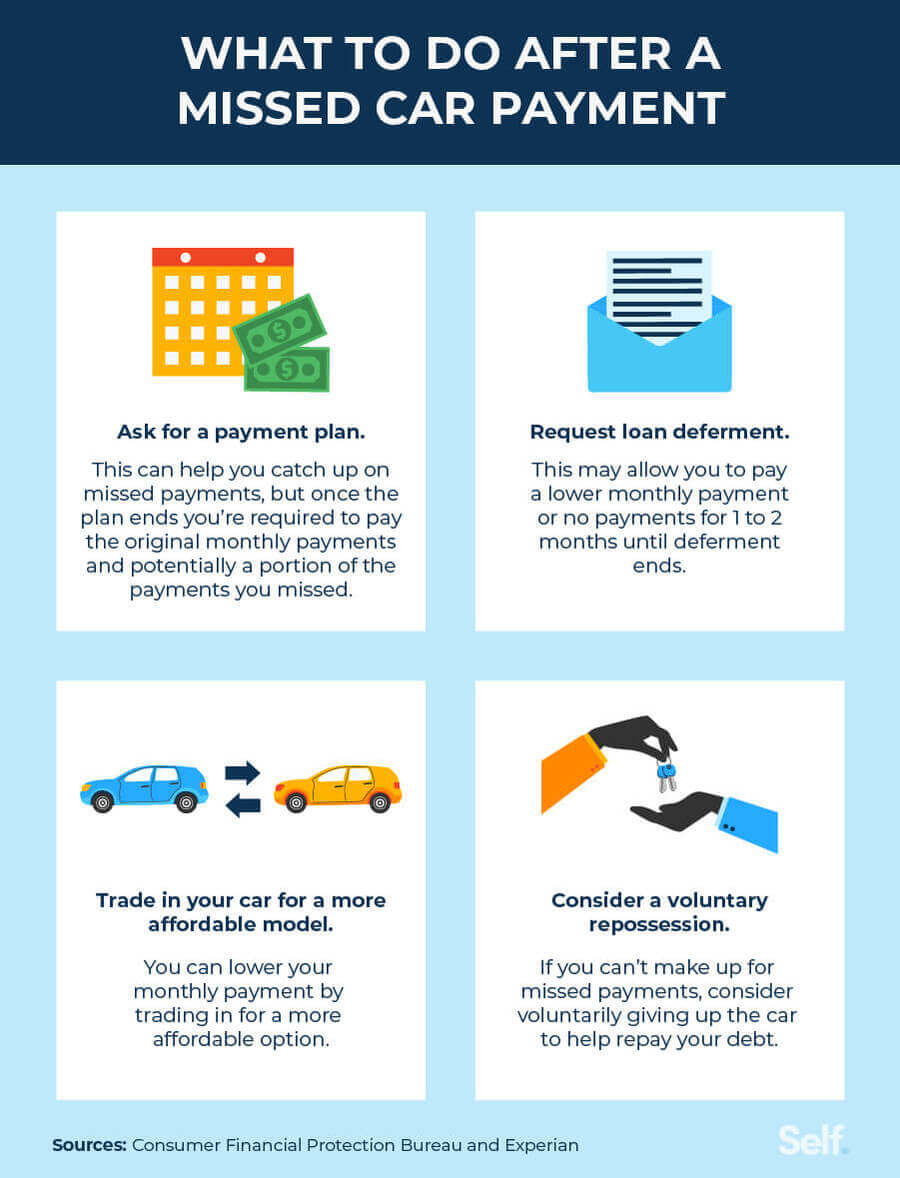

Preventing Repossession

Talk to your lender if you can’t pay. Explain your situation clearly. Show any proof of your money problems. Ask them for more time to pay. They might agree to a new plan de pago. This can help you avoid losing your car. Remember, lenders want their money back. They may agree to help you. Be polite and honest when you talk to them. It makes a good impression.

Refinancing means getting a new loan to pay the old one. This can lower your monthly pagos. First, check if you qualify for refinancing. Not everyone can get it. Compare different lenders’ offers. Look for the lowest interest rate. A lower rate means less money to pay back. Think about the loan term too. A longer term means smaller payments. But you might pay more in total. Choose the best option for your situation.

Rebuilding After Repossession

Credit repair can feel hard after repossession. Paying bills on time is key. It shows you can manage money. Revise su informe de crédito for mistakes. Fix any errors quickly. Crear un presupuesto to stay on track. It helps you control spending. Save money each month. Even small amounts help.

Talk to creditors if you struggle. They might offer new payment plans. Consider credit counseling for guidance. Experts provide advice on debt and spending. They offer support and tips. Paciencia is crucial. Credit repair takes time.

Planning for the future is smart. Set clear goals for savings. Emergency funds are vital. They cover surprises. Invest wisely if possible. It grows your money slowly. Budget for fun too. Enjoy life responsibly.

Track spending weekly. It prevents overspending. Learn about finance. Books and courses help. Stay informed about money trends. Avoid risky choices. Be consistent with savings and spending. It builds a strong future.

Preguntas frecuentes

How Many Missed Payments Lead To Repossession?

Typically, missing three consecutive payments can lead to repossession. However, this varies by lender and contract terms. Some lenders may initiate repossession after just one missed payment. Always review your loan agreement for specific details. It’s crucial to communicate with your lender if you’re facing financial difficulties.

Can A Car Be Repossessed After One Missed Payment?

Yes, a car can be repossessed after one missed payment. Many lenders have the right to repossess after a single default. However, it’s more common after multiple missed payments. It’s important to read your loan agreement. Reach out to your lender to discuss possible solutions if you’re struggling.

What Should I Do If I Miss A Payment?

Contact your lender immediately if you miss a payment. Explain your situation and ask for possible options. Some lenders may offer payment extensions or modified terms. Acting quickly can prevent further penalties and repossession. Open communication is key to finding a resolution.

Can Late Fees Prevent Repossession?

Late fees alone typically do not prevent repossession. They are additional charges for missed payments. However, timely payment of late fees can help maintain a positive relationship with your lender. It’s crucial to address the underlying issue of missed payments to avoid repossession.

Conclusión

Understanding car loan terms is crucial. Missing payments can lead to repossession. Always communicate with your lender if you’re struggling. They might offer solutions. Set reminders to avoid missing payments. Remember, repossession affects your credit score. Keep track of your payment schedule.

Budget wisely to meet your commitments. Seek advice if financial troubles arise. Being informed helps you make better decisions. Stay proactive in managing your loan.