¿Es posible obtener un préstamo sobre el título del vehículo y seguir pagando? ¡Descubre cómo!

Are you juggling car payments and wondering if you can still secure a title loan? You’re not alone.

Many people find themselves in situations where extra cash is needed, but the car isn’t fully paid off yet. The good news is that getting a title loan while still making payments is possible, and it might just be the financial solution you’re seeking.

We’ll dive into how title loans work, what lenders typically look for, and the steps you can take to maximize your chances of approval. Stick around, because understanding this process could unlock a new level of financial flexibility for you.

Title Loans Explained

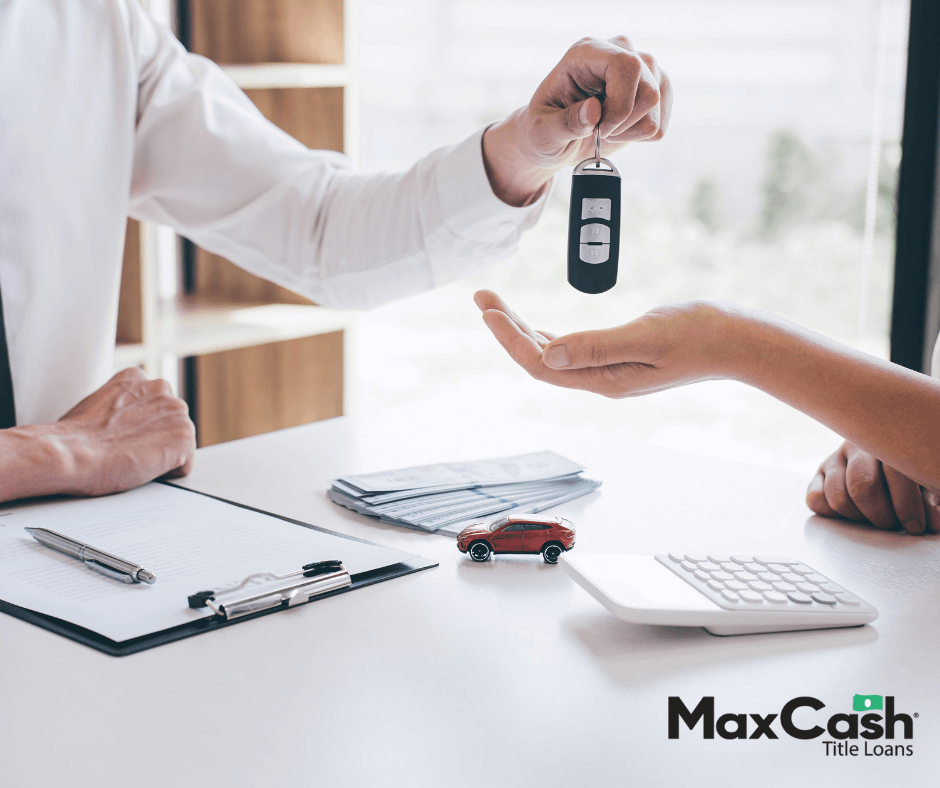

A title loan lets you borrow money using your car as security. The lender keeps the car title until you pay back the loan. You can still drive your car while paying the loan. These loans are short-term and usually have high interest rates.

It’s important to know that missing payments can lead to losing your car. Lenders can take your car if you don’t pay. People often choose title loans for quick cash needs. They are easier to get than other loans.

Understanding title loans is crucial. These loans can help but also have risks. Always read the terms carefully before getting a title loan.

Requisitos de elegibilidad

To get a title loan, you must meet some basic criteria. You should be at least 18 years old. You also need a valid government-issued ID. A steady income source is necessary too. Lenders want to know you can make payments. A clear vehicle title is important. This means no other loans on the car. Your car should be in your name. If it’s not, you might face issues. These are the main things lenders check.

Credit score is less important for title loans. Many people worry about credit scores. But for title loans, it’s not a big deal. Lenders focus more on the value of your car. They also look at your ability to pay. So, even with a low credit score, you can still apply. Bad credit won’t stop you. Focus on having a good vehicle title. This is what lenders care about most.

Title Loans Vs. Car Payments

Title loans and car payments are not the same. Title loans use your car as a collateral. This means the lender can take your car if you don’t pay. Car payments are monthly costs to own the car. Both need money each month, but they are separate.

Paying both a title loan and car payment is possible. You must be careful with your money. Calculate your monthly income. Then, check your bills. Make sure you can pay both. If not, you may face trouble. Missing payments can lead to losing your car. Always think before you take a title loan. It is very important.

How To Apply For A Title Loan

You need important papers for a title loan. Car title is the most important. It proves you own the car. Proof of income shows you can pay back the loan. ID card is also needed. It shows who you are. Insurance papers might be required. Some places need these for safety.

Visit a lender who offers title loans. Bring all your documents. The lender will check them. Fill out an application form. Write details about yourself and your car. Wait for approval. It might take a few hours. If approved, you get the money. Pay the loan back in time. Keep up with payments. This keeps your car safe.

Risks And Considerations

Borrowing more money can lead to more debt. It is easy to forget about tasas de interés. These can add up quickly. Make sure you can pay on time.

Missing payments can affect your credit. This may make future loans harder to get. You could also lose your car if you cannot pay. This is a big risk.

List your debts to see what you owe. Prioritize paying off the most important ones first. Try to make small extra payments if you can. This helps reduce debt faster.

Avoid new loans if possible. Focus on what you already owe. Make a presupuesto to track where your money goes. This helps control spending.

Opciones alternativas

Refinancing helps adjust loan terms to better fit your needs. This option might lower your interest rate. It can also extend your payment period. You can keep your car while changing your loan. It’s an option many people choose. It helps manage monthly payments easier. It can offer better financial control.

| Tipo de préstamo | Beneficios |

|---|---|

| Préstamo personal | Can be used for any purpose. Often has lower interest. |

| Payday Loan | Quick cash option. Short repayment period. |

| Tarjeta de crédito | Easy to use. Flexible payment options. |

Tips For Successful Loan Management

Create a presupuesto that lists all monthly bills. Include your loan payment. Make sure you know how much is left after bills. Save some money for emergencies. Use the rest wisely. Cut costs when you can. Avoid buying things you don’t need. Every dollar counts.

Pay your loan on time. Missing payments can lead to losing your car. Talk to your lender if you struggle. They might help you with a new plan. Keep your lender informed always. Protect your car and your credit score. It’s important to stay proactive.

Preguntas frecuentes

Can I Get A Title Loan With Existing Car Payments?

Yes, you can get a title loan while making car payments. Lenders assess your car’s equity and loan balance. If there’s enough equity, they may approve your application. It’s crucial to ensure you can manage both loans to avoid financial strain.

What Happens If I Default On A Title Loan?

If you default, the lender can repossess your car. Communicate with your lender if you’re facing payment issues. Some lenders offer payment plans or extensions. Repossession is a last resort, but it’s best to avoid it through proactive communication.

How Does A Title Loan Affect My Credit Score?

Title loans generally don’t affect your credit score directly. Most lenders don’t report to credit bureaus. However, if your car is repossessed, it can impact your financial stability. Always aim to repay on time to avoid any indirect consequences on your credit.

Are There Alternatives To Title Loans?

Yes, there are alternatives such as personal loans or credit union loans. These options might offer lower interest rates and better terms. Consider borrowing from friends or family as a last resort. Evaluate all options to find the best fit for your financial situation.

Conclusión

Exploring title loans while still paying off your car? Yes, it’s possible. But, it’s crucial to weigh the pros and cons. Understand the terms and fees involved. Always communicate with your current lender. This helps avoid any potential issues. Loan terms can vary widely.

So, do your homework. Research different lenders for the best deal. Remember, borrowing more means more responsibility. Make sure you can handle it. Choose wisely to avoid financial stress. Your decision should support your financial health. Stay informed and consider your options carefully.